The shipments component of the Cass Freight Index rose 0.5% m/m in November, after two consecutive declines.

Ongoing economic growth and slowing private fleet capacity additions are helping to narrow the y/y declines, but the normal seasonal pattern would have the index down about 3% y/y in December.

After rising 13% in 2021 and 0.6% in 2022, the index declined 5.5% in 2023 and is on track for a 4% decline in 2024.

See the Methodology for the Cass Freight Index

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, rose 0.9% m/m in November. The y/y decline moderated to 3.8% from 5.9% in October.

With shipments up 0.5% m/m, we infer the 0.9% increase in expenditures included rates up 0.4% m/m in November in the third straight price increase.

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index fell 19% in 2023, after a record 38% surge in 2021 and another 23% increase in 2022. It declined another 16% in 1H’24, and assuming the normal seasonal pattern in December, will decline 11% this year.

The rates embedded in the two components of the Cass Freight Index rose 0.4% m/m in November, and 0.4% in SA terms too.

Based on the normal seasonal pattern, this index will still fall 3%-4% y/y in November. The normal seasonal pattern from here would leave inferred rates down 7%-8% in 2024, with a small upward turn in Q1’25.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index rose 0.8% m/m in November, the third straight small increase from a cycle low in August.

See the Methodology for the Cass Truckload Linehaul Index

The U.S. GDP-based ACT Freight Composite is on track to rise 3.2% in 2024, reflecting the goods economy broadly. Using the Cass Freight Index as a proxy for the for-hire sector, we can infer private fleet volume growth of roughly 6% for most of the past year, slowing recently as the declines in for-hire shipments moderate. In this context, the 4% decline that the Cass Freight Index is headed toward in 2024 implies a roughly 5% increase in private fleet volumes.

Private fleets continue to show a surprising willingness to add capacity despite wider than normal cost disadvantages, which makes more sense in the context of significant equipment cost increases ahead in 2027. Although private fleets may continue to limit demand in the for-hire market, for-hire activity will likely benefit from slowing private fleet growth and temporary pre-tariff shipping in 1H’25.

The chart below has been on the back burner for a while as the noise caused by a large LTL bankruptcy played through. But, as a new MIT/C.H. Robinson study shows, modal mix is a helpful cyclical indicator. And the increase we can see in Cass LTL mix (which has continued past the y/y lapping of Yellow’s July 2023 demise) suggests higher for-hire demand and rates to come.

Our outlook through 2026 is detailed in the ACT Research Freight Forecast. This service provides in-depth analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, DAT spot and contract rates by trailer type, LTL, and intermodal price indexes. We provide monthly, quarterly, and annual predictions for over forty data series over a two- to three-year time horizon, including capacity, volumes, and rates. The ACT Research Freight Forecast is released monthly in conjunction with the Cass Transportation Index report.

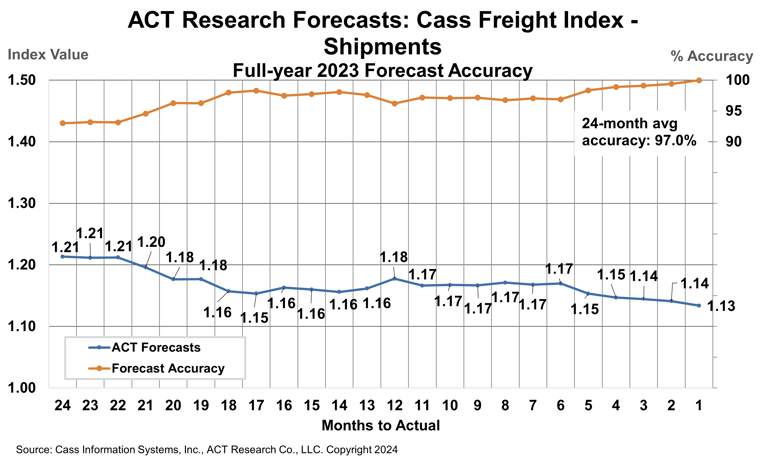

How have ACT Research’s freight forecasts performed? For 2023, ACT’s forecasts for the shipments component of the Cass Freight Index were 96.9% accurate on average for the 24-month forecast period.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

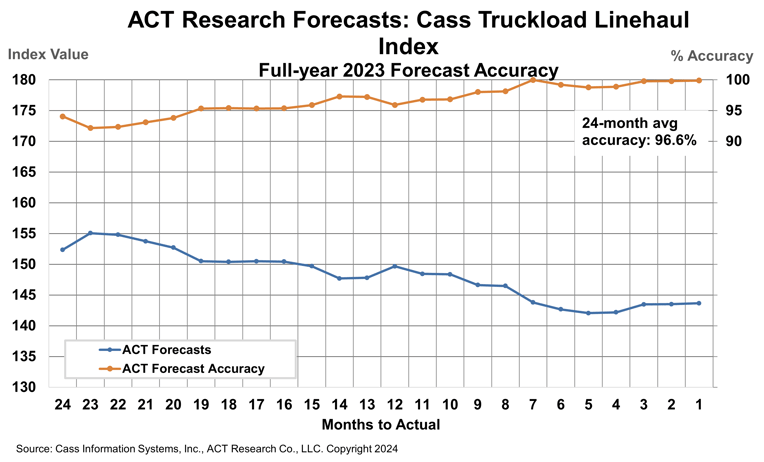

ACT Research’s 2023 forecasts for the Cass Truckload Linehaul Index were 96.6% accurate on average over the past 24 months, and 98.5% accurate over the past 12 months. The Cass Truckload Linehaul Index averaged 143.8 in 2023, precisely in line with our July 2023 estimate.

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.