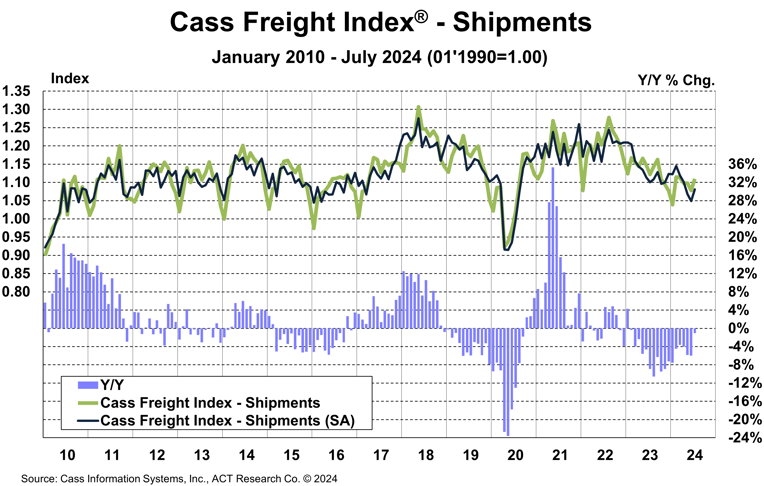

The shipments component of the Cass Freight Index rose 3.0% m/m in July, after four straight declines.

Goods demand continues to grow slowly, but private fleet capacity additions are slowing, which appears to be reducing the pressure on for-hire shipments.

After rising 0.6% in 2022, the index declined 5.5% in 2023. With normal seasonality, the index will fall about 3% y/y in August and about 4% for the full year.

See the Methodology for the Cass Freight Index

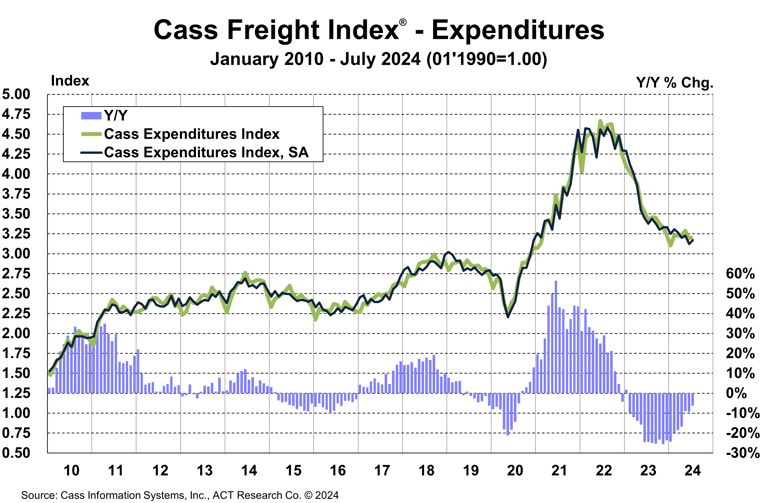

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, rose 0.7% m/m in July. The 6.2% y/y decline narrowed from a 9.4% drop in June.

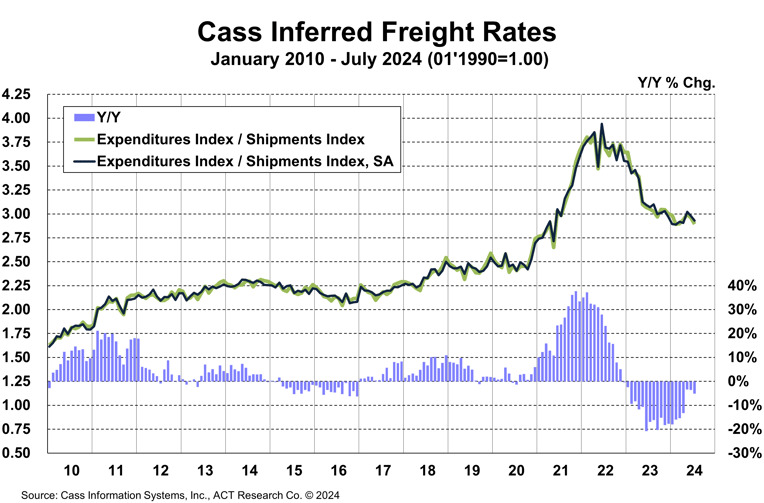

With shipments up 3.0% m/m, we infer from the smaller 0.7% rise in expenditures that rates were down 2.2% m/m in July (see our inferred rates data series below).

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index fell 19% in 2023, after a record 38% surge in 2021 and another 23% increase in 2022. It declined another 16% in 1H’24, and assuming normal seasonal patterns from here, will decline about 11% this year.

The rates embedded in the two components of the Cass Freight Index declined 5.2% y/y in July, after a 3.6% y/y drop in June.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index fell 1.0% m/m in July for the second straight month as the soft market balance persists and overcapacity keeps bids highly competitive.

See the Methodology for the Cass Truckload Linehaul Index

The bounce in the Cass Freight Index (shipments) coincides with lower Class 8 sales. Private fleet capacity additions, insourcing, and increased spot activity have been dragging out the for-hire downturn for at least a year. We’ve been surprised at the magnitude of prebuying over the past year, and our U.S. Class 8 tractor forecasts don’t suggest much capacity tightening, but it appears equipment supply is moderating.

For-hire fleets have tightened their belts, with the publicly traded TL fleets we track operating 6.6% fewer tractors than last year in Q2. The low returns on investment at these rates suggest low equipment demand, and private fleets are insourcing into uncompetitive costs, which can’t last indefinitely.

After significant overbuying in the past two years, Class 8 tractor sales have normalized, and we see a lull in prebuying taking shape as cost economics return to the fore over the next year. Uncertainty about the election and interest rates is likely to delay decision making for some months, as manufacturers’ backlogs have thinned. And as one fleet manager explained to us recently, there are fewer and fewer post-pandemic catch-up replacements.

Our outlook through 2026 is detailed in the ACT Research Freight Forecast. This service provides in-depth analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type, LTL, and intermodal price indexes. ACT Research provides monthly, quarterly, and annual predictions for over 40 data series over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast is released monthly in conjunction with the Cass Transportation Index report.

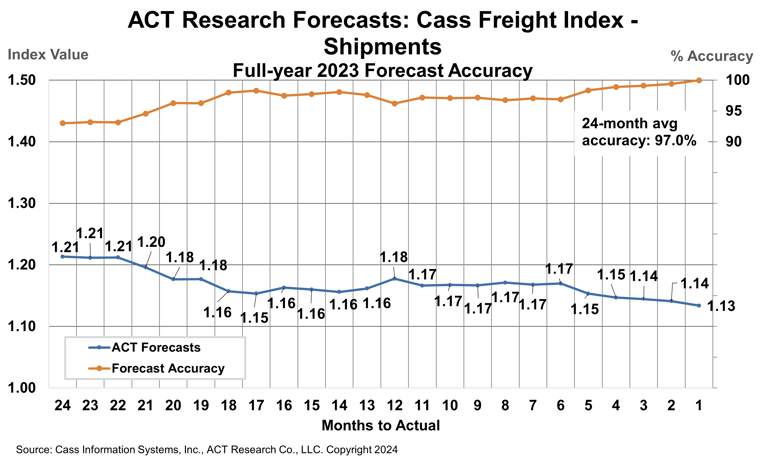

How have ACT Research’s freight forecasts performed? For 2023, ACT’s forecasts for the shipments component of the Cass Freight Index were 96.9% accurate on average for the 24-month forecast period.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

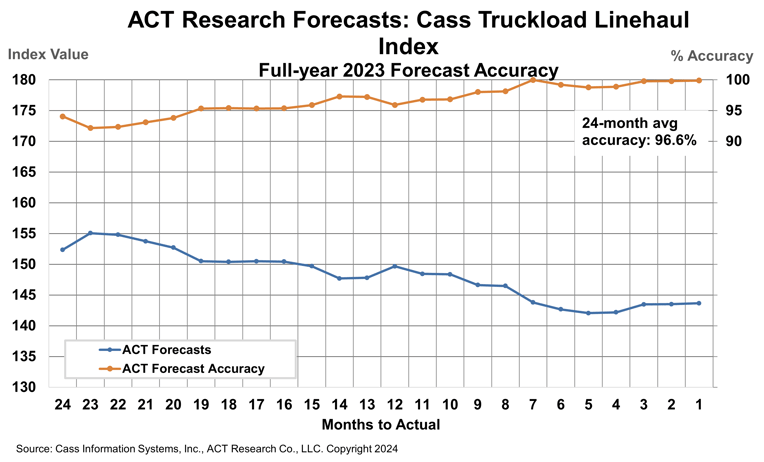

ACT Research’s 2023 forecasts for the Cass Truckload Linehaul Index were 96.6% accurate on average over the past 24 months, and 98.5% accurate over the past 12 months. The Cass Truckload Linehaul Index averaged 143.8 in 2023, precisely in line with our July 2023 estimate.

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.