The shipments component of the Cass Freight Index fell 1.7% m/m in September, after a 1.0% increase in August.

In a sign that private fleet insourcing still isn’t finished, the decline comes as Class 8 tractor sales jumped in Q3 after supply constraints in Q2.

After rising 13% in 2021 and 0.6% in 2022, the index declined 5.5% in 2023. With normal seasonality, the index will fall about 3% y/y in October and 4%-5% in 2024.

See the Methodology for the Cass Freight Index

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, rose 2.4% m/m in September despite another decline in fuel prices. The y/y decline in expenditures moderated to 6.6% from 9.0% in August.

With shipments down 1.7% m/m, we infer the 2.4% increase in expenditures included rates up 4.2% m/m in August (see our inferred rates data series below).

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index fell 19% in 2023, after a record 38% surge in 2021 and another 23% increase in 2022. It declined another 16% in 1H’24, and assuming normal seasonal patterns from here, will decline 11%-12% this year.

The rates embedded in the two components of the Cass Freight Index declined 1.4% y/y in September, after a 7.2% y/y drop in August.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index—a measure of the movement in linehaul rates—rose 0.3% m/m in September, the first increase after four straight monthly declines.

See the Methodology for the Cass Truckload Linehaul Index

The key theme we’ve been highlighting for more than a year now is the insourcing of freight from the for-hire market to private fleets, which has perhaps been the defining feature extending the soft freight cycle in an economy that has surpassed expectations. The resilience of owner-operators is of course an important part of the story, but operating authority revocations continue apace.

Lower equipment supply, particularly by private fleets, may play a key role in a market turn in 2025, in our view. And next month, an FMCSA regulation could potentially downgrade tens of thousands of CDL holders in states who have not heretofore been required to enforce the FMCSA’s Drug & Alcohol Clearinghouse.

This is a tough one to quantify. Our industry contacts suggest there is definitely some number of drivers in violation on the road. Not at the large, high-quality fleets, but it’s happening. See a recent Q&A here. When state driver’s license authorities downgrade a large number of CDLs on November 18th, it should have two measurable effects: making our roads safer, and leading truckload rates higher.

Our outlook through 2026 is detailed in the ACT Research Freight Forecast. This service provides in-depth analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, DAT spot and contract rates by trailer type, LTL, and intermodal price indexes. We provide monthly, quarterly, and annual predictions for over forty data series over a two- to three-year time horizon, including capacity, volumes, and rates. The ACT Research Freight Forecast is released monthly in conjunction with the Cass Transportation Index report.

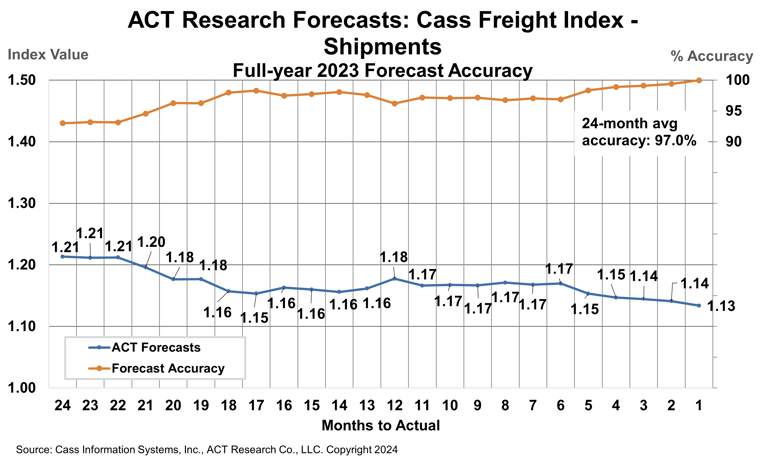

How have ACT Research’s freight forecasts performed? For 2023, ACT’s forecasts for the shipments component of the Cass Freight Index were 96.9% accurate on average for the 24-month forecast period.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

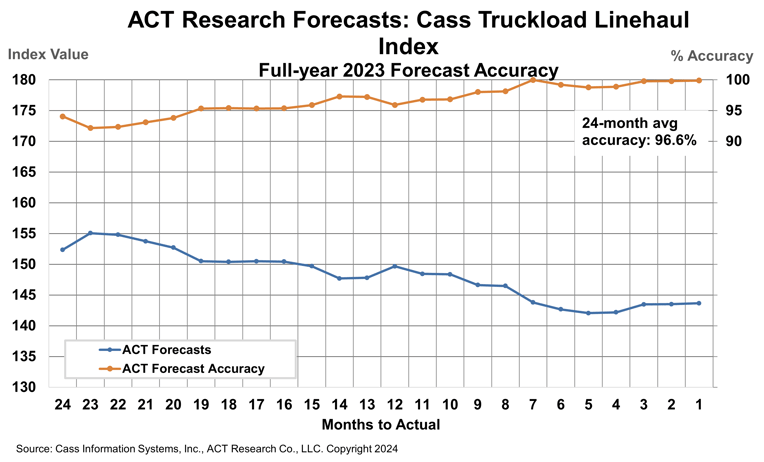

ACT Research’s 2023 forecasts for the Cass Truckload Linehaul Index were 96.6% accurate on average over the past 24 months, and 98.5% accurate over the past 12 months. The Cass Truckload Linehaul Index averaged 143.8 in 2023, precisely in line with our July 2023 estimate.

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.